Focus is on funding from the infrastructure law and the Inflation Reduction Act.

Source: New feed

Focus is on funding from the infrastructure law and the Inflation Reduction Act.

Source: New feed

Vantage Data Centers is planning a three-building campus in New Albany, Ohio, where several other data center projects are also being developed.

Source: New feed

Firm steps up to complete the critical transportation project after China Harbor and Engineering Co. Ltd. exited the project last year over financing issues.

Source: New feed

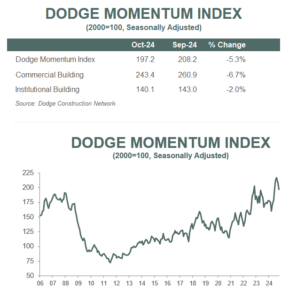

Slower planning across several segments drove weaker activity this month.

BEDFORD, M.A. – November 7, 2024 — The Dodge Momentum Index (DMI), issued by Dodge Construction Network, decreased 5.3% in October to 197.2 (2000=100) from the revised September reading of 208.2. Over the month, commercial planning fell 6.7%, and institutional planning declined 2.0%.

“In addition to data center planning normalizing, a moderate pullback in the number of planning projects for several other nonresidential sectors also contributed to the decline in the Dodge Momentum Index for October,” stated Sarah Martin, associate director of forecasting at Dodge Construction Network. “Regardless, owners and developers remain confident in next year’s market conditions, and the planning queue remains poised to spur stronger construction activity in 2025, following deeper rate cuts by the Fed.”

Most commercial categories faced declines throughout October, aside from hotel planning – which continued to gain momentum. On the institutional side, education and public planning activity expanded, offset by weaker activity in healthcare, recreational, and religious projects.

This month, the DMI was 13% higher than in October of 2023. The commercial segment was up 18% from year-ago levels, while the institutional segment was up 3% over the same period. The influence of data centers on the DMI this year has been substantial. If we remove all data center projects from January to October, commercial planning would be down 4% from year-ago levels, and the entire DMI would be down 2%.

A total of 18 projects valued at $100 million or more entered planning throughout October. The largest commercial projects included $450 million EdgeCloudLink Data Center in Houston, Texas and the $410 million GFT Hotel in Arlington, Texas. The largest institutional projects to enter planning were the $300 million Kellogg School Building at Northwestern University and the $270 million Primrose School of Stevens Ranch in San Antonio, Texas.

The DMI is a monthly measure of the value of nonresidential building projects going into planning, shown to lead construction spending for nonresidential buildings by a full year.

The post Dodge Momentum Index Retreats 5% in October appeared first on Dodge Construction Network.

Source: New feed

A second Trump administration will have impacts on energy and environmental policy, from an expected restart of construction on LNG export terminals to a broader realignment in permitting and regulatory approaches.

Source: New feed

Some ballot measures approved by voters will put billions of dollars toward various construction projects, while others could clear—or add—red tape.

Source: New feed

ENR’s 20-city average cost indexes, wages and materials prices. Historical data and details for ENR’s 20 cities can be found at ENR.com/economics

Source: New feed

With projections showing former President Donald Trump has retaken the presidency, the focus for construction observers now turns to the final tally in Congress.

Source: New feed

Many races were still unsettled as of late night on Election Day.

Source: New feed

Nuclear plant owner says an initial 300 MW of data center development can proceed despite federal regulator’s rejection of grid link agreement to its facility in Pennsylvania.

Source: New feed