Year-end surge prevails against high rates and limited credit accessibility

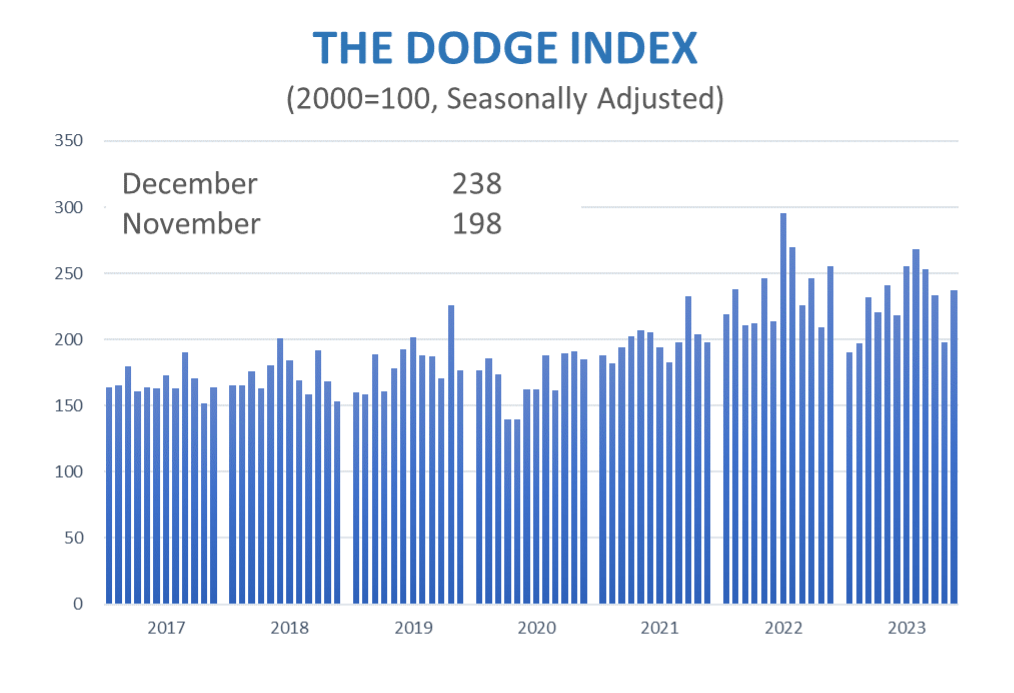

BEDFORD, MA —January 18, 2024 — Total construction starts grew 20% in December to a seasonally adjusted annual rate of $1.12 trillion, according to Dodge Construction Network. Nonresidential building starts rose 37% during the month, while residential starts gained 8% and nonbuilding starts improved by 13%.

For the full year of 2023, total construction starts lost 4% compared to the previous year. Residential and nonresidential starts were down 13% and 8%, respectively, but nonbuilding starts were up 16%.

“Construction starts ended the year on a positive note,” said Richard Branch, chief economist for Dodge Construction Network. “Looking ahead, the new year provides promise that positive momentum will continue to build. The planning queue is stabilizing, and the promise of lower rates should spur construction onward. While hurdles remain, including scarce labor and tight credit, 2024 should be a more positive year for the construction sector.”

Nonbuilding

Nonbuilding construction starts in December rose 13% to a seasonally adjusted annual rate of $253 billion. Starts were up in each category; miscellaneous nonbuilding starts gained 27%, utility/gas plants rose 15%, highway and bridge starts improved by 12%, and environmental public works were up 8%. For the full year 2023, nonbuilding starts were up by an overall 16%. Utility/gas plants rose 35% and miscellaneous nonbuilding starts increased 19%. Highway and bridge starts and environmental public works each rose 9%.

The largest nonbuilding projects to break ground in December were the $1.3 billion Faraday Solar project in Elberta, Utah, the $425 million San Juan 1 solar farm in Farmington, New Mexico, and the $300 million renovation of the David Booth Kansas Memorial Stadium in Lawrence, Kansas.

Nonresidential

Nonresidential building starts rebounded in December, gaining 37% from November to a seasonally adjusted annual rate of $479 billion. Manufacturing starts gained 75%, commercial starts rose 48% with all categories seeing sizeable gains. Institutional starts rose 22% with increases in education, public buildings, and recreation offsetting a decline in healthcare starts. In 2023, total nonresidential starts were 8% lower than in 2022. Institutional starts gained 7%, while commercial and manufacturing starts fell 12% and 27%, respectively.

The largest nonresidential building projects to break ground in December were the $2.7 billion Texas Instruments fabrication plant in Sherman, Texas, the $1.1 billion OxyChem Project Orca in La Porte, Texas, and the $815 million University of Chicago Cancer Center in Chicago, Illinois.

Residential

Residential building starts grew 8% in December to a seasonally adjusted annual rate of $391 billion. Single family starts increased 1%, while multifamily starts rose 22%. In 2023, total residential starts were down by 13%, with single-family starts dropping 13%, and multifamily starts by 12%.

The largest multifamily structures to break ground in December were the $430 million Auberge South Beach Condo project in Miami Beach, Florida, the $325 million 2600 Biscayne mixed-use project in Miami, Florida, and the $300 million mixed-use project at 55 Hudson St in Jersey City, NJ.

Regionally, total construction starts in December rose in the Midwest, South Atlantic, and West regions, but fell in the Northeast.

Watch Chief Economist Richard Branch discuss December Construction Starts here.

December 2023 Construction Starts

The post Construction Starts Grow 20% in December appeared first on Dodge Construction Network.

Source: New feed