After a strong March, April shows marginal slowdown overall

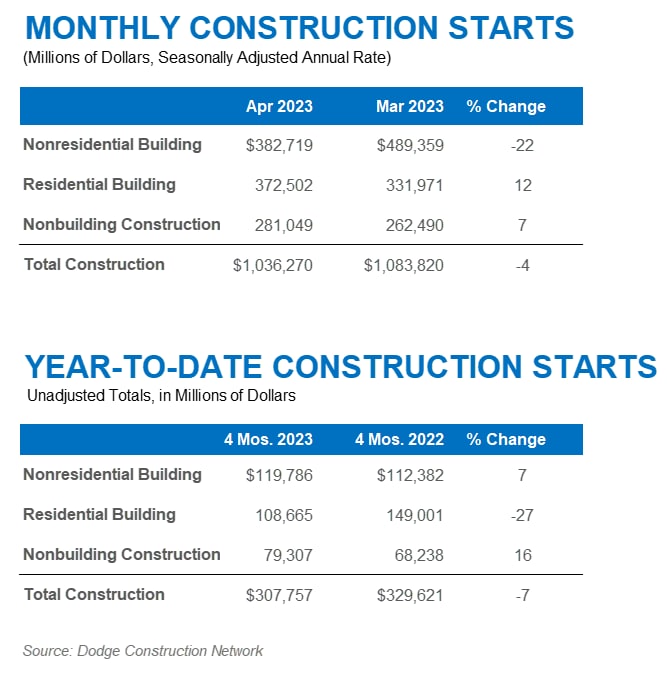

HAMILTON, NJ —May 18, 2023 — Total construction starts fell 4% in April to a seasonally adjusted annual rate of $1.04 trillion, according to Dodge Construction Network. Nonresidential starts led the drop as manufacturing fell 22% following strong performance in March. To balance the decline, nonbuilding starts rose 7%, and residential building starts gained 12%.

On a year-to-date basis through April, total construction starts were 7% below the first four months of 2022. Residential starts were down 27%, and nonresidential and nonbuilding starts grew 7% and 16%, respectively. For the 12 months ending April 2023, total construction starts were 11% higher than the 12 months ending April 2022. Nonresidential and nonbuilding starts both showed gains at 34% and 24%, respectively; however, residential starts hindered overall growth with a 13% decline on a 12-month rolling basis.

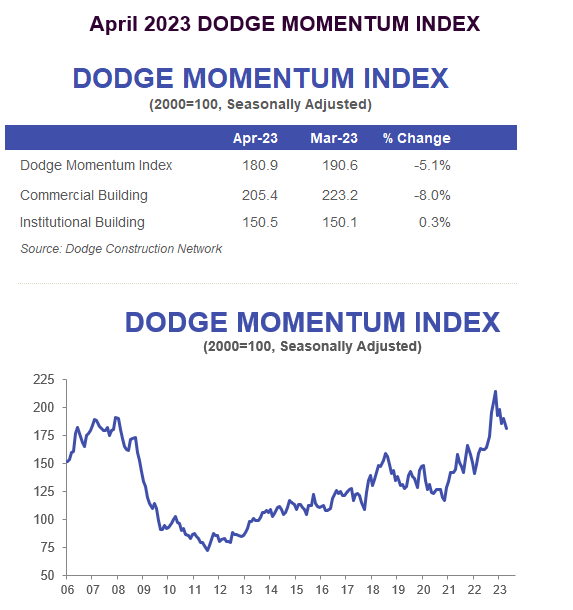

“The construction sector continues to sweep its economic worries under the rug, even with inflation, unstable banking, and the potential breach of the U.S. debt ceiling,” said Richard Branch, chief economist for Dodge Construction Network. “While the presence of, or lack thereof, large manufacturing projects each month has made the data more volatile, the underlying trends point to a very healthy sector. However, this is likely transitory. The Dodge Momentum Index, which tracks projects entering the earliest stages of planning, is falling, which should lead to weaker starts in the second half of the year – especially for the private sector.”

Nonbuilding

Nonbuilding construction starts improved 7% in April to a seasonally adjusted annual rate of $281 billion. The utility/gas plant category had the largest gain in the month, rising 76%, with a small increase in street and bridge starts at 5%. Miscellaneous nonbuilding starts fell 16%, and environmental public works lost 17%. Year-to-date through April, nonbuilding starts gained 16%. Utility/gas plants rose 37%, and miscellaneous nonbuilding starts were up 36%. Environmental public works rose 10%, and highway and bridge starts gained 9%.

For the 12 months ending April 2023, total nonbuilding starts were 24% higher than the 12 months ending April 2022, with significant gains across each sector. Utility/gas plant starts rose 43%, miscellaneous nonbuilding starts were 27% higher, highway and bridge starts were up 20%, and environmental public works rose 17% on a 12-month rolling sum basis.

The largest nonbuilding projects to break ground in April were the $750 million Magnolia Power/Kindle Energy generating station in Plaquemine, Louisiana, the $738 million Rock Creek wind farm in Laramie, Wyoming, and the $542 million Eagle LNG export facility in Jacksonville, Florida.

Nonresidential

Nonresidential building starts declined 22% in April to a seasonally adjusted annual rate of $383 billion. This sharp decline follows an equally large in March, when numerous large manufacturing plants took off. In April, manufacturing starts lost a staggering 68%. Institutional starts dropped 13%, largely due to a pullback in healthcare construction, while commercial starts improved 5% thanks to an increase in retail and office construction. Year-over-year, in January 2023 through April 2023, total nonresidential starts were 7% higher than in the first four months of 2022. Institutional starts gained 14%, manufacturing starts were 4% higher, and commercial starts were up 2%.

Between April 2022 and April 2023, total nonresidential building starts were 34% higher than April 2021 through April 2022. Manufacturing starts were 118% higher, institutional starts improved 22%, and commercial starts gained 18%.

The largest nonresidential building projects to break ground in April were the $1.2 billion Hanwha Qcells solar plant manufacturing plant in Cartersville, Georgia, the $650 million Group14 battery plant in Moses Lake, Washington, and the $600 million Mutual of Omaha headquarters in Omaha, Nebraska.

Residential

Residential building starts increased 12% in April to a seasonally adjusted annual rate of $373 billion. Single family and multifamily starts remained strong, increasing 14% and 10%, respectively. On a year-to-date basis through April 2023, total residential starts were down 27%. Single family starts were 34% lower, and multifamily starts were down 10%.

For the 12 months ending in April 2023, residential starts were 13% lower than that ending in April 2022. Single family starts were 25% lower, while multifamily starts were up 14% on a rolling 12-month basis.

The largest multifamily structures to break ground in April were the $549 million Mana’olana Place mixed-use building in Honolulu, Hawaii, a $500 million mixed-use building in Flushing, New York, and the $385 million 710 Broadway Apartments in Santa Monica, California.

Regionally, total construction starts in April fell in the Midwest, South Atlantic, and South Central regions, but rose in the Northeast and West.

Watch Chief Economist Richard Branch discuss April Construction Starts here.

April 2023 CONSTRUCTION STARTS

The post Total Construction Starts Slip in April Due to Sharp Decline in Manufacturing appeared first on Dodge Construction Network.

Source: New feed

About Dodge Construction Network

About Dodge Construction Network